by Randall Bartlett and Alex Reeves

One year out from the 2019 federal election, and the battle lines are being drawn. Corporate income tax (CIT) rate cuts in the US have challenged Canada’s business tax advantage, and the pressure is on for the federal government to respond in the Fall Economic Statement. And then you have the federal carbon tax, the constitutionality and rationality of which is being challenged by several provincial governments and by every federal party on the right of the political spectrum. Beyond taxes, there is also the issue of the glacial pace at which infrastructure dollars have been flowing, resulting in large lapses. Add to that the flood of red ink spilled on the federal government’s fiscal forecasts, and Canadians should be prepared to be served up a spicy medley of rhetoric and public policies as Budget 2019 and election platforms are prepared.

In the beginning, there were accountants

But before looking ahead to the fiscal policies that may be, it’s important to look at where the Government of Canada’s revenue and spending numbers are today and where they’ve been. To do that, one needs to look no further the audited financial statements of the federal government known as the Public Accounts of Canada.

It is the Public Accounts of Canada 2017-2018 (Public Accounts) and the federal government’s head accountant – the Auditor General of Canada (AG) – that have taken center stage recently. This is because, in its Annual Financial Report of the Government of Canada 2017-2018 (AFR), the federal government finally gave way to prior recommendations from the AG to change the interest rate at which future unfunded pension liabilities are discounted. Talk about a mouthful, the details of which will be the subject of an upcoming report by the Institute of Fiscal Studies and Democracy (IFSD).

But this accounting changed is conceptually not all that complicated. Essentially, all of the future liabilities – pension and other benefits – that the federal government will owe past, present, and future public servants are divided each year by an interest rate, known as the discount rate. (This is done because most of us rationally discount future events more than those that are staring us in the face. And the further into the future an event is, the less we worry about it still.) These annual discounted amounts are then added together to get the total future liability for account purposes, known as the accrued benefit obligation.

Specific to the recent accounting change, the AG wanted the federal government to use the long-term Government of Canada bond yield at the end of the prior year as opposed to the 20-year moving average, it’s prior convention. This meant using a lower interest rate to discount future liabilities. And the lower the discount rate is, the higher is the accrued benefit obligation because the future liabilities are divided by a smaller number. (In contrast, the higher the discount rate is, the lower is the accrued benefit obligation because the future liabilities are divided by a bigger number.)

It was the move to using a lower discount rate through this accounting change that took most of the headlines when the AFR was recently published. That’s because of the impact this change had on historical debt and deficit estimates, with deficits being pushed further in the red due to higher operating expenses associated with more elevated public service benefits. Taking the changes into account during the decade through the 2017-18 fiscal year, the average impact on the budget balance was to lower it by $1.9 billion annually, increasing the size of historical deficits. Of course, the impact of the accounting change varied from year-to-year, most notably in fiscal 2014-15, where the federal government had previously recorded a surplus of $1.9 billion but is now a deficit of $0.6 billion (Chart 1).

This accounting change has also caused the federal debt to be revised higher. It is now estimated to have been $671.3 billion in the 2017-18 fiscal year, which is $20.1 billion higher than would have been the case in the absence of the accounting change (Chart 2). As a result of the upward revision, the debt-to-GDP ratio is also higher by 0.9% than would otherwise have been the case, thereby hitting 31.3%. It’s important to note that, regardless of the discount rate used, the debt-to-GDP ratio fell back in the 2017-18 fiscal year after rising in the prior two fiscal years.

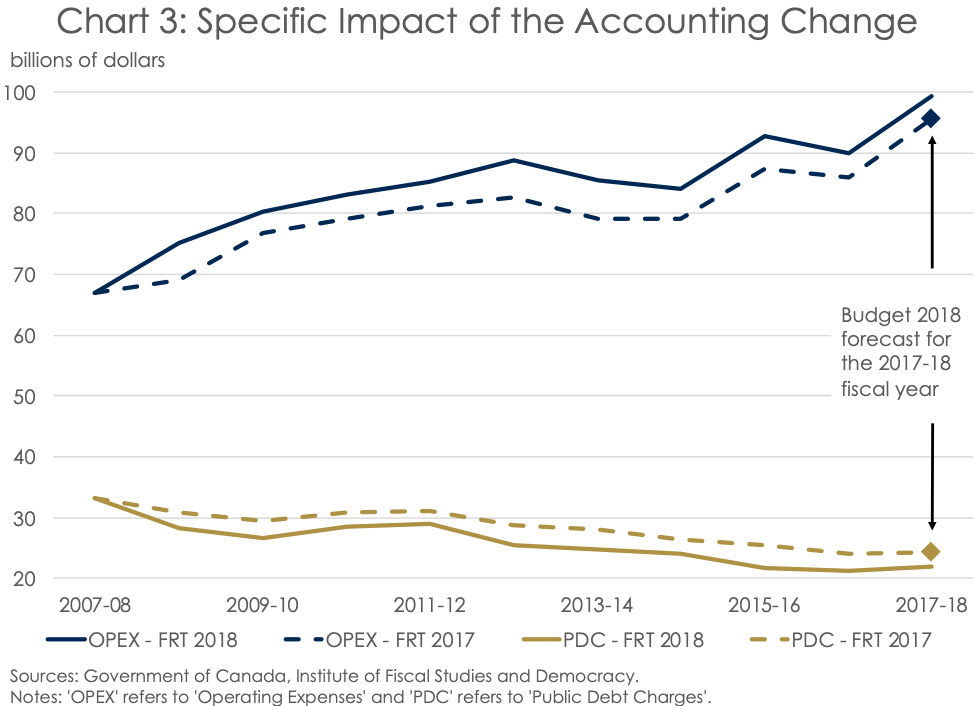

Given this accounting change only impacted future federal government obligations to public servants, the upward revisions were jammed into operating expenses. And these discretionary expenses have changed considerably since the Public Accounts were last released in September 2017 (Chart 3). On average, starting in the 2008-09 fiscal year, operating expenses have now been revised up $4.9 billion annually relative to what was report a year ago. Notably, while the lower discount rate for future liabilities has increased operating expenses, it has had the opposite effect on public debt changes, which have fallen by $2.8 billion on average annually starting in fiscal 2008-09.

But try to scratch beneath the surface of operating expenses just a little bit, say to the level of individual departments, and things start to get pretty murky. For instance, in the Fiscal Reference Tables 2018 – which provide annual data on the financial position of the federal, provincial-territorial and local governments – the federal government has stopped reporting on spending by crown corporations and on national defence. It has also stopped reporting on these items in the monthly federal Fiscal Monitor, making in-year spending by the Department of National Defence (DND) impossible to track relative to its commitment in the Defence Policy Review. And given the impact that the accounting change has on pensions and benefits, of which DND is a major player, holding the Government of Canada’s feet to the fire on military spending just got that much more complicated. Thankfully, the federal Department of Finance has been kind enough to provide several months of National Defence data to start the 2018-19 fiscal year which has allowed for some benchmarking, albeit very limited (Chart 4).

It’s important to keep in mind, though, that the federal government has provided additional information in the Fiscal Monitor starting in April 2018 on total expenses by object of expense, such as personal, professional and special services, etc. However, the limited time series of this data and the recent accounting changes mean this data will have little usefulness in scrutinizing federal spending for the foreseeable future.

And the Magic Eight Ball says …

So, with changes to accounting and reporting practices by the federal government when it comes to operating expenses, the IFSD’s established process for forecast operating expenses has had to be revisited. Thankfully, the IFSD’s approach is based on expense object in a manner similar to the new Fiscal Monitor reporting framework, so the change in the accounting convention when it comes to discount rates can be incorporated in the near term. Instead, the difficulty comes into play over the longer term, as today’s low interest rates are expected to rise over the forecast, thereby putting further downward pressure on future public-sector liabilities (Chart 5).

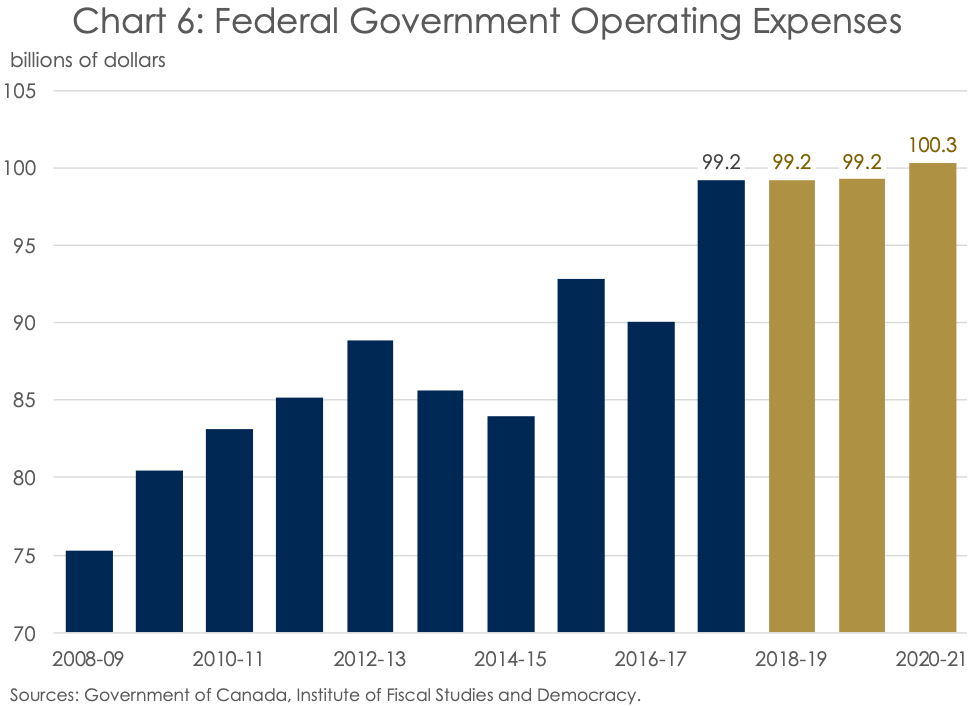

Of course, where there’s a will, there’s a way, and the IFSD has used a combination of information from the Receiver General, Departmental Plans, Public Accounts, and Fiscal Monitor to produce a forecast for operating expenses which is consistent with all of these sources (Chart 6). As can be observed, operating expenses are expected to be relatively stable going forward. This, in part, reflects a rising discount rate suppressing the cost of future benefits while the full-time equivalent (FTE) count is expected to fall after hitting its peak in fiscal 2018-19.

But the calm on the surface of the IFSD’s operating expense forecast masks greater volatility beneath. Specifically, spending on federal personnel – the largest single operating expense category – is expected to fall consistently after the 2017-18 fiscal year (Chart 7). In fiscal 2018-19, this is entirely because greater expenditures on wages and salaries, on the back of increased FTEs, are expected to be more than offset by falling liabilities associated with pensions and benefits. After the 2018-19 fiscal year, spending on wages and salaries should stabilize as a slightly lower FTE count is offset by modest wage gains. And as the discount rate applied to future pension and benefit liabilities moves higher, the contribution to the personnel bill from these spending categories will gradually diminish further, with this decline more than offsetting the modest advances in wages and salaries. As such, the increase in the IFSD’s operating expense forecast presented in Chart 6 can be tied to rising non-personal operating expenses, such as utilities and professional services, and capital spending.

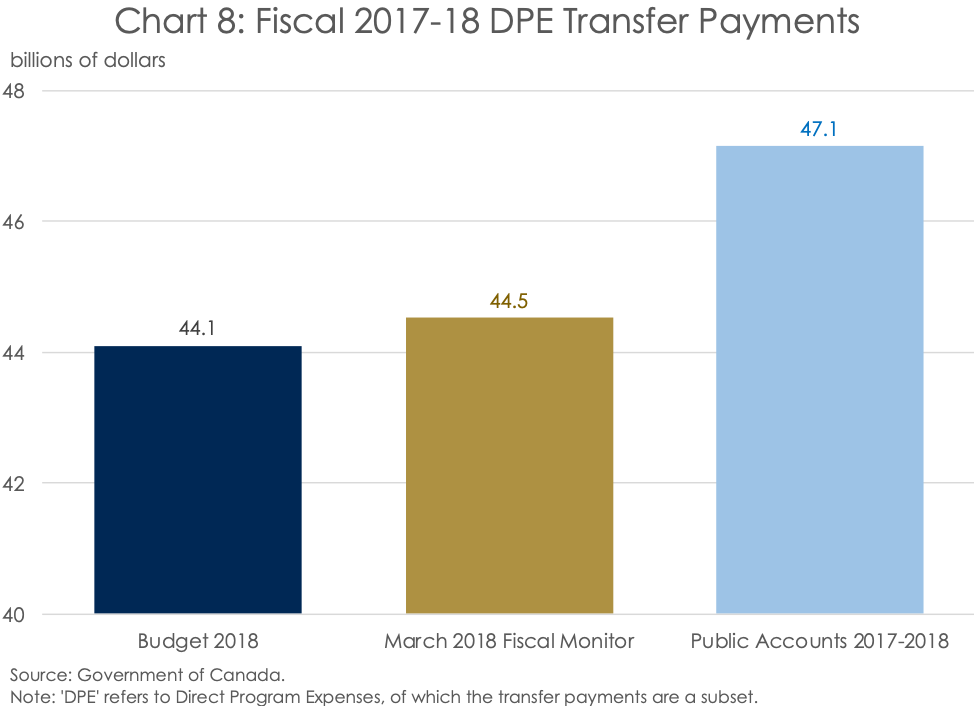

However, transfer payments are the other component that make up Direct Program Expenses (DPE), and these have been relatively volatile themselves. For example, transfer payments came in $3 billion higher in the 2017-18 fiscal years once the numbers had been tallied than was anticipated in Budget 2018 (Chart 8). That is almost 7% beyond what was expected in the budget, and has nothing to do with changes in accounting practices. So, what’s driving this difference? According to the AFR, this reflects “increases across a number of departments and agencies, including increased assistance for students, transfers under the new Early Learning and Child Care Program, transfers to First Nations and infrastructure transfers.” As such, for simplicity, we’ve taken on the federal government’s transfer payment profile under DPE from Budget 2018 starting in the 2018-19 fiscal year, as the IFSD had done in its June 2018 Federal Fiscal Forecast.

Of course, questions remain around how much of the increase in transfer payments can be chalked up to an unexpected increase in infrastructure spending in the 2017-18 fiscal year. More specifically, Budget 2018 was published on February 27, 2018, over one month before the end of the fiscal year. And given infrastructure spending is reported only when receipts are received from other levels of government (known as a modified-cash basis of reporting), that gap in time may have allowed more receipts to roll in than was anticipated when the budget was published. But this line of reasoning is suspect, as the March 2018 Fiscal Monitor reported transfer payments of $44.5 billion, only $0.4 billion more than was projected in the budget (Chart 8). Indeed, construction receipts from the other levels of government should have been long accounted for by the time the March 2018 Fiscal Monitor was published at the end of May 2018. As such, it’s tough to directly attribute the higher transfer payments in the Public Accounts to infrastructure.

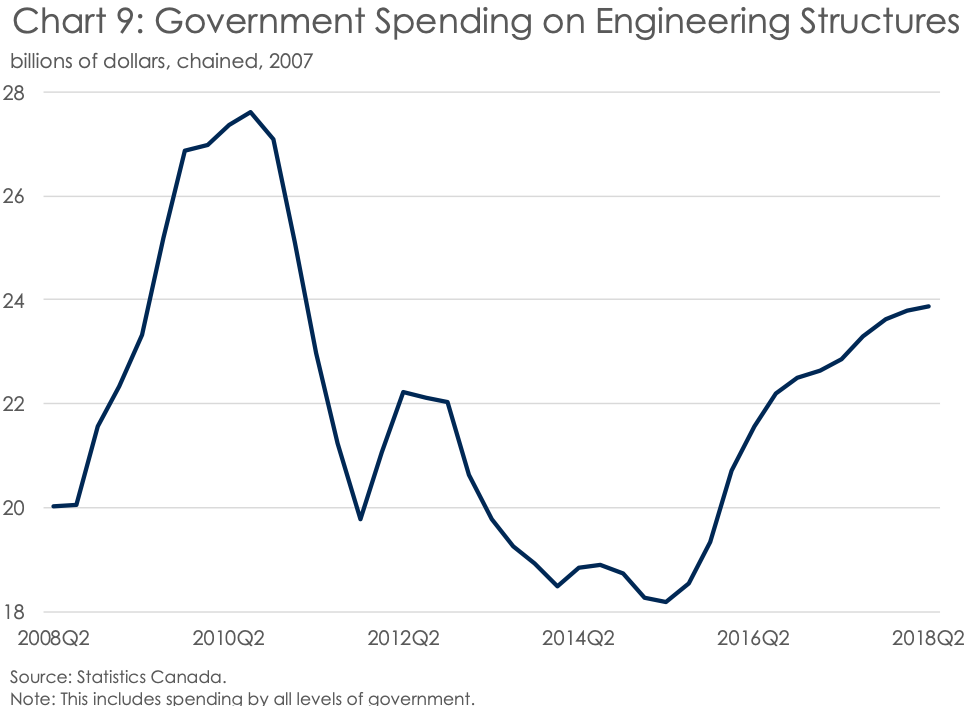

But, when it comes to infrastructure, there are a couple of things we do know. First, infrastructure dollars are flowing, as evidenced by the sharp increase in total government investment in engineering structures (roads, bridges, and the like) since bottoming out in 2015Q2 (Chart 9). As the IFSD argued recently in its analysis of monetary policy in Canada, these dollars are flowing at a time of plenty, and they may turn out to more inflationary and interest-rate-hike inducing than growth stimulating as a result. Second, despite this unfortunate inflation-inducing consequence of fiscal largesse, the Prime Minister assigned the new Minister of Infrastructure, Francois-Philippe Champagne, the thankless task in his Mandate Letter of getting the money out the door even faster. We call this a thankless task as infrastructure lapses, by the nature of how the money is granted and receipts remitted, are more the rule than the exception under all federal governments. And the data from Infrastructure Canada suggest this trend isn’t about to change any time soon (Chart 10).

Combining transfer payments and operating expenses to get DPE, it can be observed that DPE is the major driver of difference in expenses between the Government of Canada and IFSD. In contrast, the differences in projected expenditures on ‘Major transfers to persons’ and ‘Major transfers to other levels of government’ are comparatively minor. Indeed, the difference in the DPE forecasts also dwarfs the gap in the outlooks of both revenues and public debt charges, which remain negative despite both surprising on the upside in fiscal 2017-18 (Chart 11).

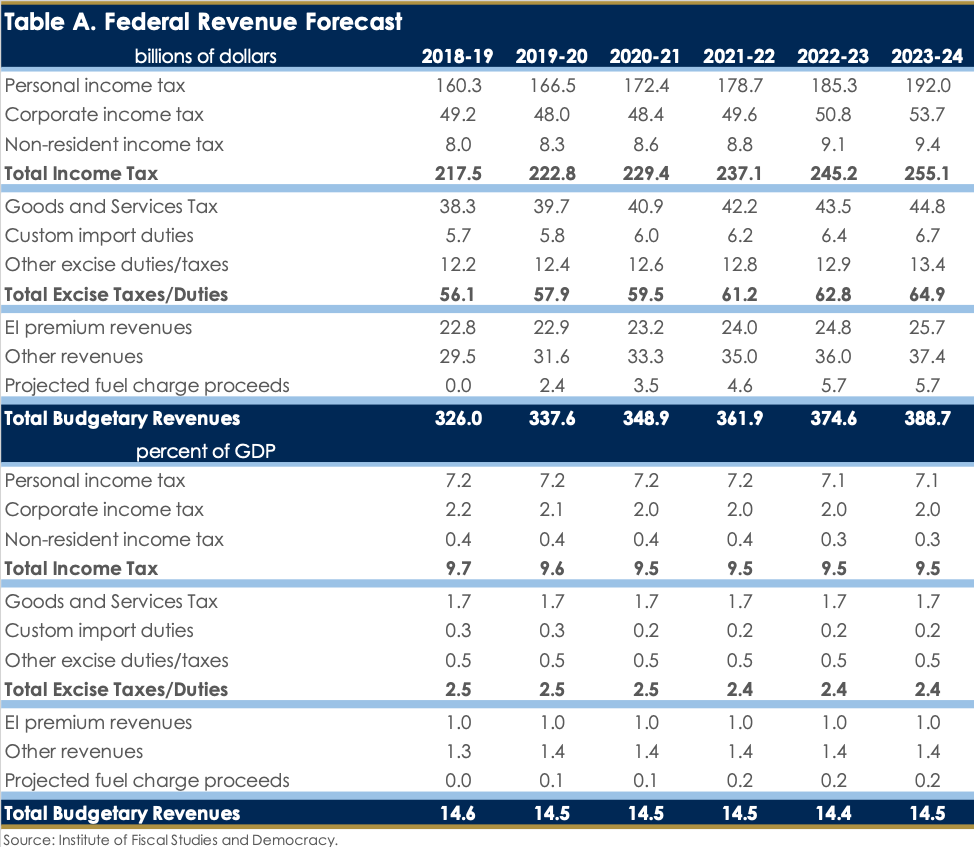

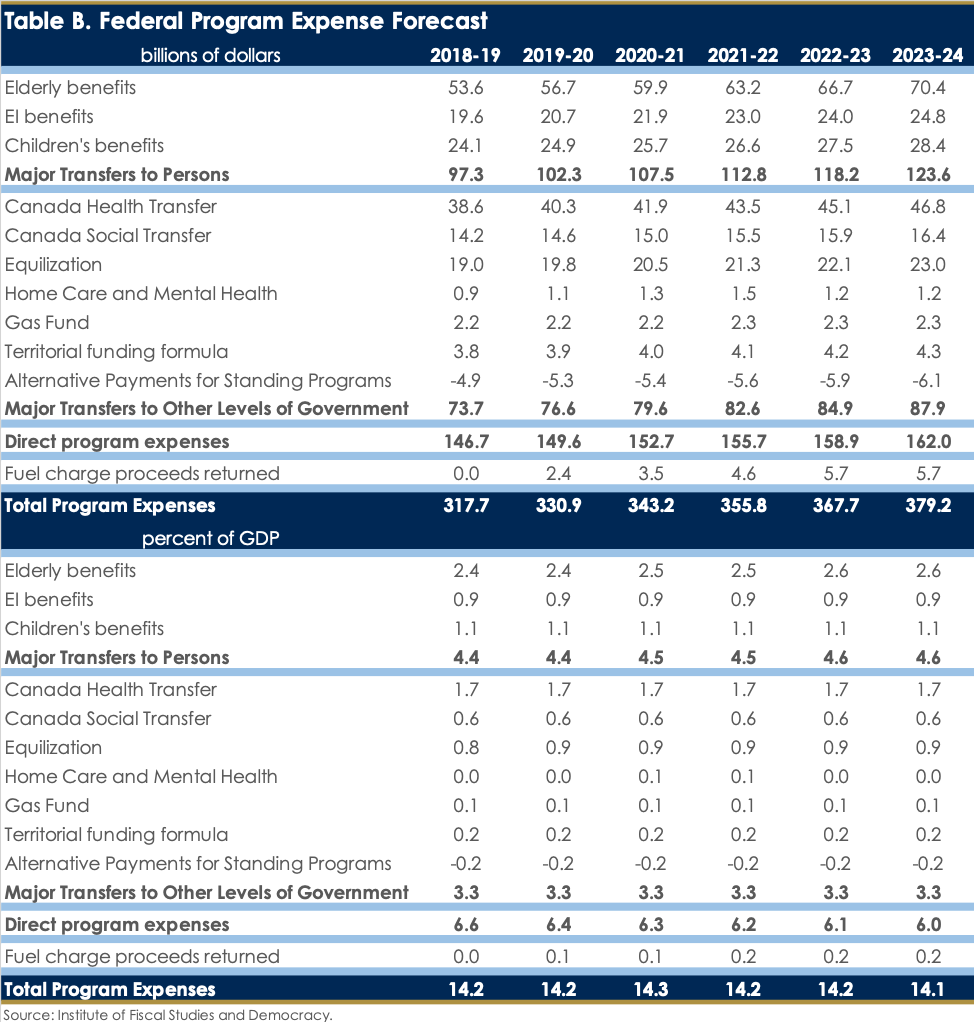

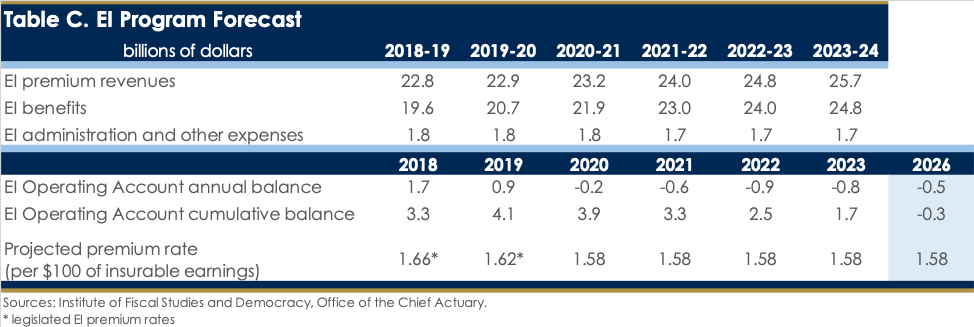

Keep in mind, in order to ensure comparability between Budget 2018 and the IFSD’s federal fiscal forecast, Chart 11 doesn’t include the recently announced federal measures around carbon pricing. Table 1 shows these measures as published on October 23, 2018, which the IFSD has incorporated into its federal fiscal forecast as presented by the Department of Finance, given the short time to publication. As a result, while both revenues and expenses have increased, these equal amounts mean that there is no impact on the deficit or level of federal debt. That said, we will provide further analysis of these measures in the run up to the federal election. Tables A through C at the end of this blogpost present the details of the IFSD’s federal fiscal forecast, including the impact of the new carbon-pricing regime.

So, where does this leave us? Ultimately, the chasm in the deficit outlooks presented in Budget 2018 and by the IFSD is substantial, as it often is (Chart 12). The IFSD does not have confidence that the federal government will be able to constrain operating expenses in a manner similar to that presented in the budget, as it has not demonstrated an ability to do so in the past. Instead, the IFSD thinks budget deficits will remain substantial due to higher discretionary spending and lower revenues that the optimistic outlook presented in Budget 2018.

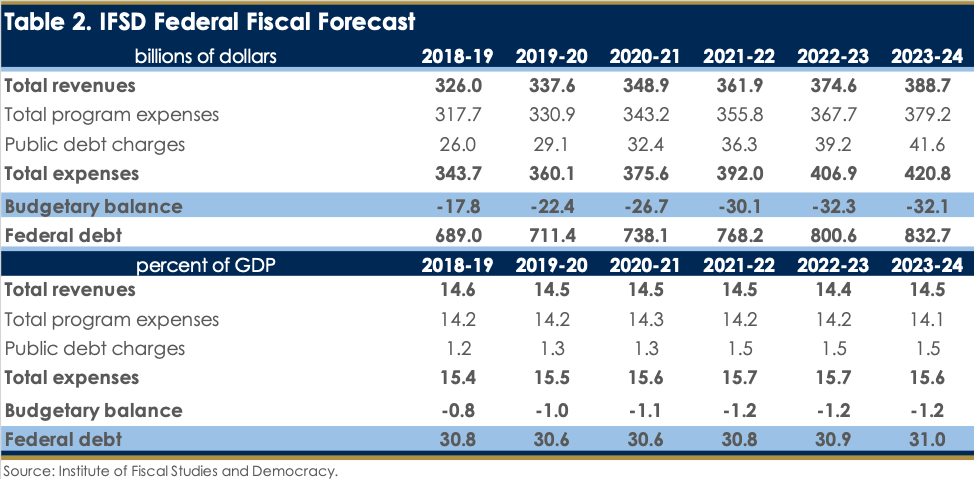

These substantial deficits also mean that the debt-to-GDP ratio is likely to move higher over the medium term (Table 2). But context matters, as it so often does. For instance, this projected rise in the debt-to-GDP ratio is modest, and is expected to decline over the long term, eventually reversing itself to such an extent that the federal government finds itself in a net asset position (Chart 13). Put simply, despite its large and seemingly endless deficits, this falling debt-to-GDP ratio implies the federal government is currently in a fiscally-sustainable position.

Unfortunately, this is a fiscal sustainability is largely the result of a reduction in the growth rate of the Canada Health Transfer as opposed to any sort of sound fiscal stewardship. Indeed, in a recent interview on Global News’ The West Block, Finance Minister Bill Morneau told the show’s host that Canada has the ‘capacity’ to handle a recession despite continued deficits. At the IFSD, we challenge this view. Our research has demonstrated that the current substantial federal deficits are entirely structural in nature, meaning there is no economic justification for running them. Further, they are also, by and large, the result of spending which is well beyond anything justified by the state of the Canadian economy. And, using this same approach, if the Canadian economy was to go into comparatively-mild recession in 2019, the federal government would see its debt-to-GDP ratio begin to rise even under its own optimistic assumptions, challenging the Finance Minister’s claim of fiscal prudence.

Conclusion

In conclusion, the federal government is increasingly painting itself into a fiscal corner. It has shown a propensity for spending the proceeds of economic windfalls in the face of substantial deficits, but these windfalls can’t be counted on to persist into the future. Instead, as the upside surprises fade, federal spending commitments will either need to be clawed back and or revenue raised, or fiscal sustainability may be put in jeopardy. This would have negative repercussion which would reverberate through to lower levels of government and Canadians more broadly. As such, going forward, the federal government should demonstrate some fiscal responsibility and reign in spending or raise more revenues to pay for it. If they don’t, we could all pay the price.