by Randall Bartlett

It was Daniel Patrick Moynihan who once said: “Everyone is entitled to his own opinion, but not his own facts.” Nowhere is this more true than in the alchemy of forecasting, where statistical models come head-to-head against old-school gut instinct. As such, there is always space for a wide range of oft-times conflicting views. And there’s no way to get around it, as even the best econometric models can’t predict an unseasonable shutdown at an automaker or an oilfield innovation leading to a rapid drop in oil prices.

But there are some things you can rely on. For one, all economists who are undertaking their forecasts at roughly the same time should be using a similar set of historical data. One would hope they would also be basing their outlooks on a similar set of priors in regard to the relationships between specific economic variables that are grounded in research.

It is for these reasons that the economic outlook presented in Budget 2018 is so perplexing. Not just because of some internal inconsistencies, which are minor. But also because of how the federal Department of Finance takes these high-level forecasts and spins them into forecasts for the underlying tax bases that the public never see and which ultimately become revenues. This lack of transparency means analysts have difficulty validating the credibility of the federal government’s revenues forecast. And “[w]ithout transparency, there can be no accountability.”

Survey Says…

Before every budget or Fall Economic Statement (FES), the federal government surveys around 15 economic shops to get a lay of the land for what will come next. However, since the federal government’s survey of economists is typically undertaken several months before the budget, it can sometimes be stale by the time its published.

Looking back to Budget 2017, as an example, it wasn’t difficult to observe at the time that the December 2016 economic forecast used was well out of date when March 2017 rolled around. Indeed, the federal government benefited from an upside surprise to revenues in FES 2017 thanks to an upwardly revised economic forecast that was predictable, at least in part, at the time of Budget 2017.

Fast forward to Budget 2018, and the tables have turned. Specifically, the December 2017 forecast that underpinned the fiscal outlook published in February 2018 is meaningfully higher than the more recent views of many Canadian economists. This suggests that the federal government’s revenue forecast in Budget 2018 is likely to be a bit on the optimistic side.

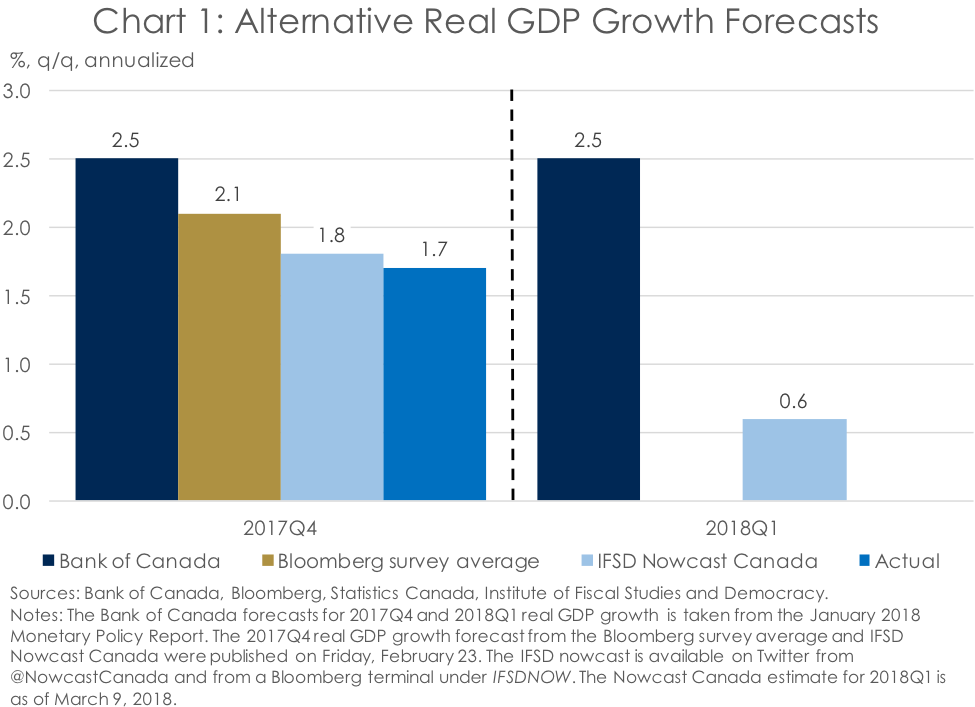

The optimism of Budget 2018’s economic outlook is that much more pronounced when one considers the string of weak economic data published since the start of 2018. And while most of this data relates to the final quarter of 2017, the trend in the data is clear. Indeed, this weakness culminated in modest advances in real GDP of 1.7% annualized in the fourth quarter of 2017, following a downward revision of third quarter growth to 1.5%. This release was well below the 2.5% expansion anticipated by the Bank of Canada in its January 2018 Monetary Policy Report (MPR) (Chart 1).

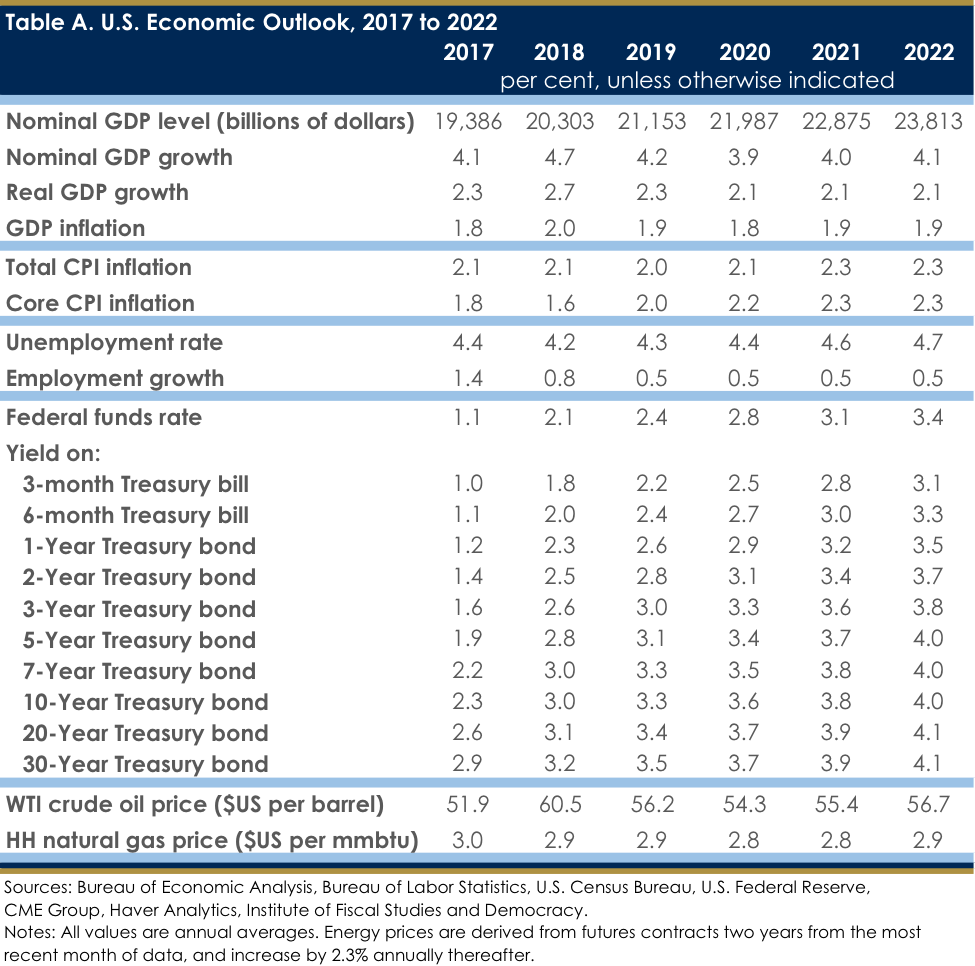

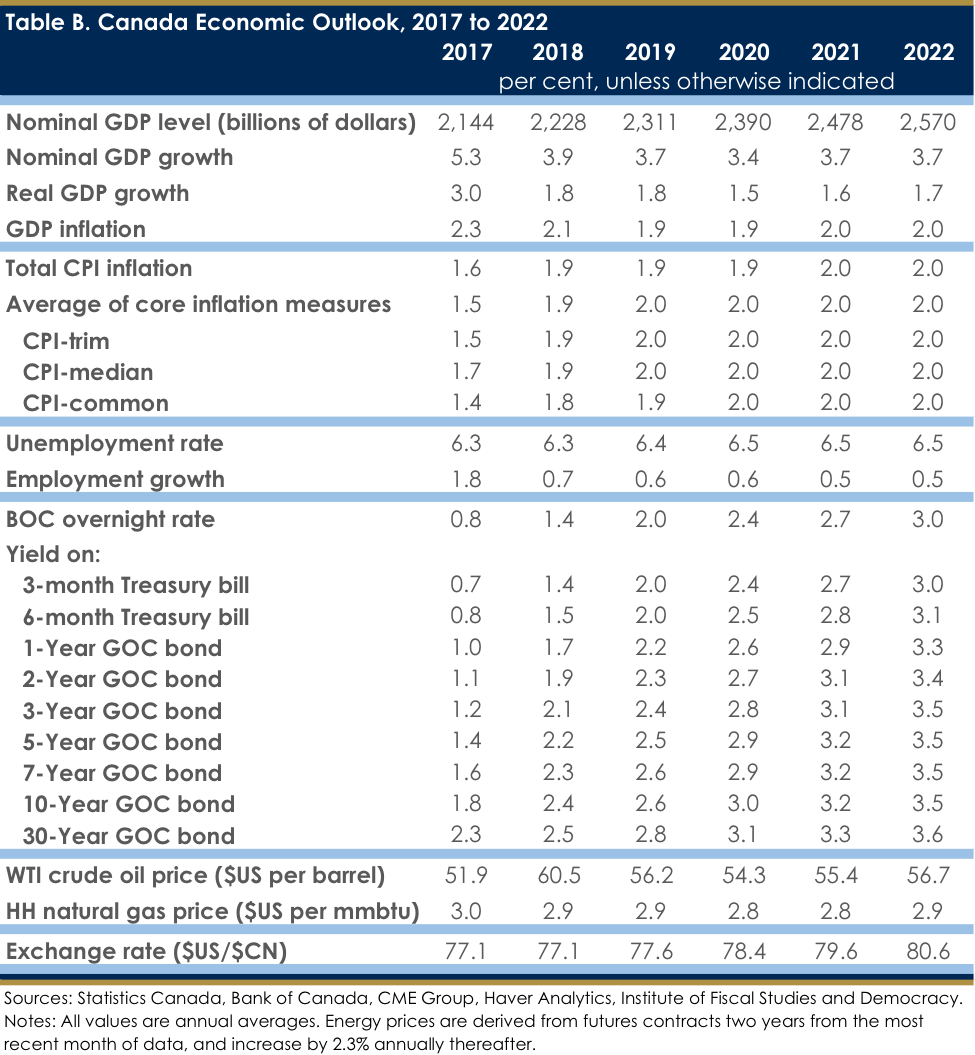

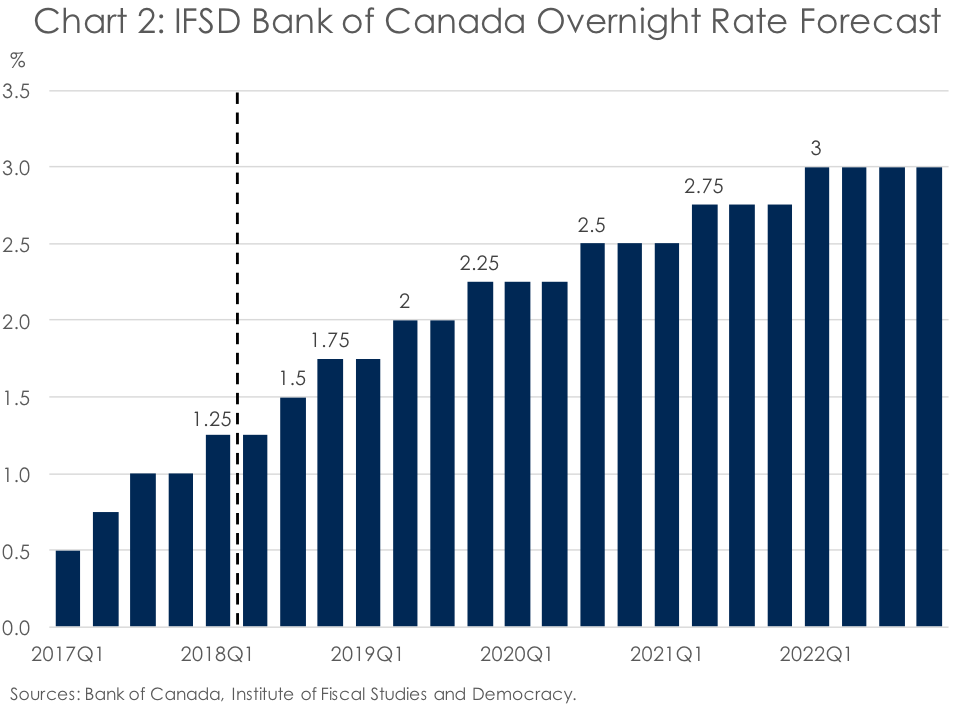

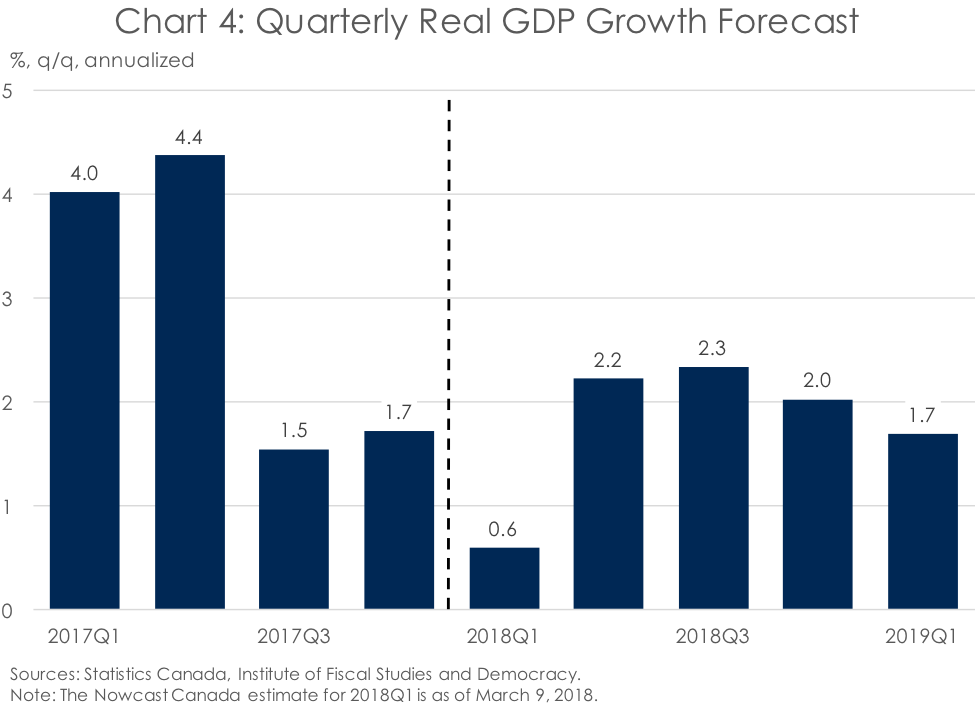

But the news gets worse. Since the economic momentum leaving 2017 was so moribund and the indicators to start this year have been so feeble, the Institute of Fiscal Studies and Democracy’s (IFSD’s) model-based nowcast, Nowcast Canada, is tracking only a slightly-positive move in real GDP growth of 0.6% annualized in the starting quarter of 2018 (Chart 1). Not only is this nothing to write home about, but this below-trend advance will give inflationary pressure a temporary reprieve and the Bank of Canada an opportunity to put rate hikes on hold for a few months. Consequently, the IFSD is expecting the Bank of Canada to hike interest rates only twice in 2018, once in the third quarter and again in the fourth (Chart 2). (See Tables A and B for the IFSD’s 5-year economic forecasts for the US and Canada, respectively.)

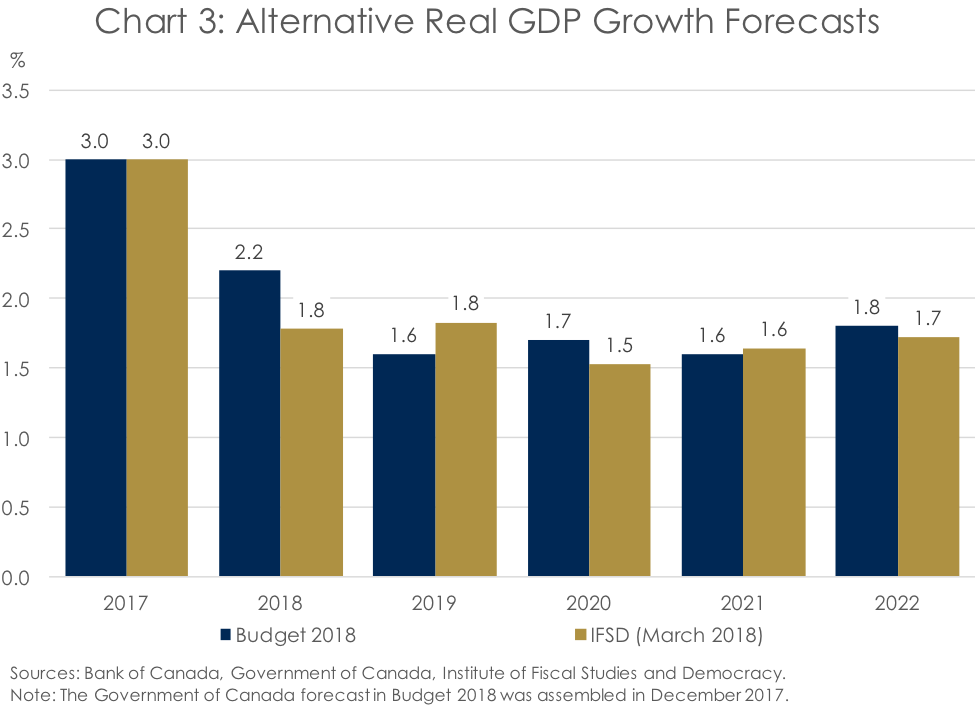

Moving beyond the starting blocks of 2018, real GDP growth this year is now expected to come in much weaker than was expected in the most recent forecasts by the federal government, Bank of Canada, or the IFSD (Chart 3). At 1.8%, the IFSD’s latest forecast for 2018 real GDP growth is a function of the weak momentum at the end of 2017 and start of 2018 combined with still above 2% annualized growth in each quarter for the remainder of the year (Chart 4). This grinding halt to the 2017 Canadian economic miracle is in large part due to a reversal in trade fortunes but also slowing consumer spending. Moreover, recently released capital and repair expenditures intentions for 2018 suggest a moderation in the growth non-residential and machinery and equipment gross fixed capital formation this year.

Economic Risks Are Tilted to the Downside

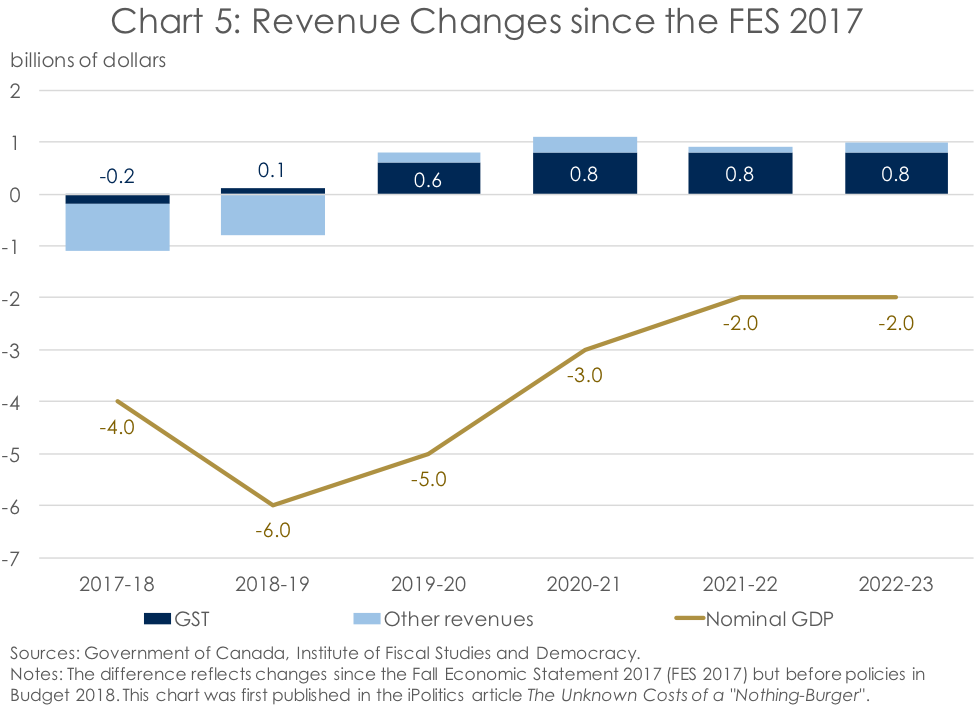

Bringing this downshift in the Canadian economy back to the outlook in Budget 2018, weaker growth is going to have major implications on federal government revenues going forward (see the IFSD’s March 2018 federal fiscal forecast for more information). But you wouldn’t know it from the budget. Indeed, most of the pre-budget-measures increase in revenues came from a higher Goods and Services Tax (GST) take than was anticipated at the time of the FES 2017. With no change in the tax rate, this points to stronger consumer spending anticipated by the feds over the coming five years. And this against the backdrop of a lower nominal GDP forecast than was published in the FES 2017 (Chart 5, originally published by iPolitics). As such, the feds’ revenue forecast doesn’t quite pass the smell test.

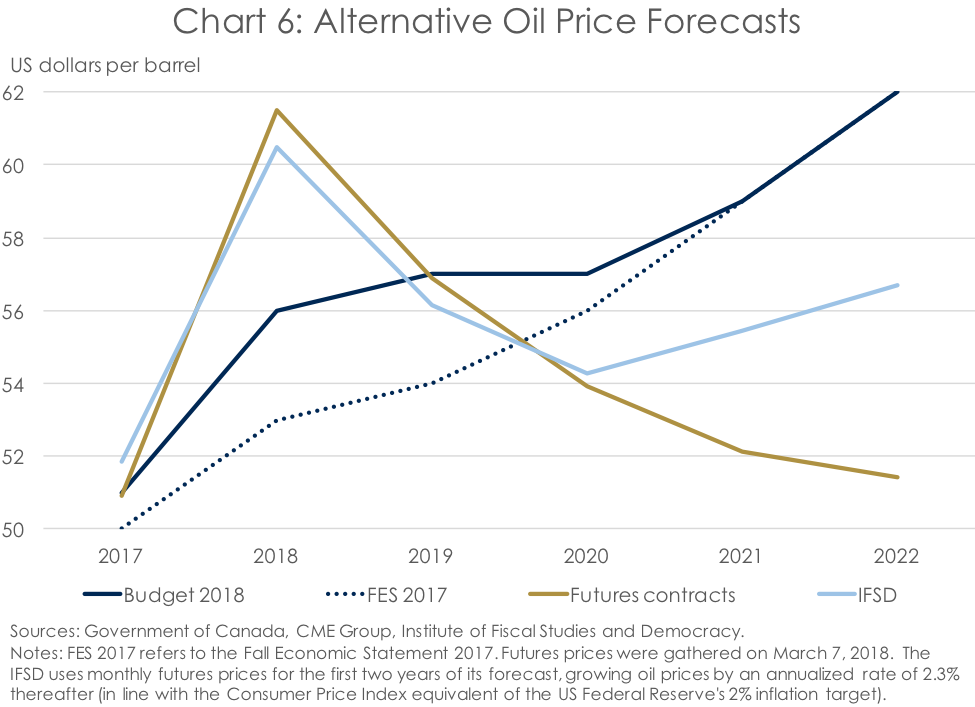

But tight-fisted consumers aren’t the only downside risk to the federal government’s economic and fiscal forecasts (despite the feds citing higher-than-expected household spending as the source of a possible upside surprise). Another area that Budget 2018 presents as a potential source of better economic results is oil prices, which the federal government feels may be higher-than-expected over the medium term due to increased demand coming up against supply constraints. Indeed, with the price of a barrel of West Texas Intermediate (WTI)––the North American light sweet crude benchmark––currently sitting around US$62 per barrel, this doesn’t seem unreasonable at first blush. However, the budget itself outlines a stark difference between the oil price projection used by the federal government and the current path of WTI-futures prices (Chart 6). Indeed, futures suggest that, while oil prices are very likely to be higher in the near term than was assumed in the budget (in fact the current price is much higher than was assumed in the budget for the current year), this upside benefit may reverse itself the further one goes out in the forecast. This is important because oil prices make a significant contribution to both real GDP growth and GDP inflation, the latter of which is the price component of nominal GDP––the broadest measure of the tax base.

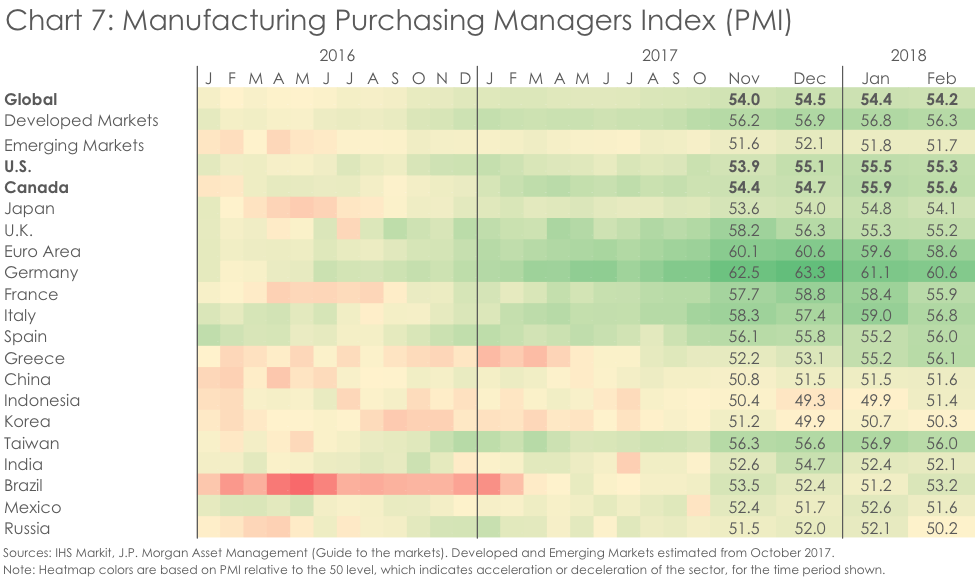

The final possibility the federal government cites as a potential source of an upside surprise is “stronger and more durable growth in the global economy than currently expected (that) would benefit Canadian economic activity.” While always possible, and certainly the extraordinary economic story of 2017, some of the early economic indicators in 2018 suggest global growth may have plateaued (Chart 7). As such, a further acceleration in growth may be wishful thinking, especially as inflation continues to rise and interest rates normalize around the world.

And these are just the downside risks to the possible upside surprises cited in Budget 2018. Other risks include uncertainties around the North American Free Trade Agreement (NAFTA) negotiations, particularly in light of the tariffs on US steel and aluminum imports recently introduced by the Trump administration, as well as high levels of household debt and the effects of rising global interest rates across the yield curve. Put these all together and you have a recipe for an economic and revenue forecast which is overly optimistic.

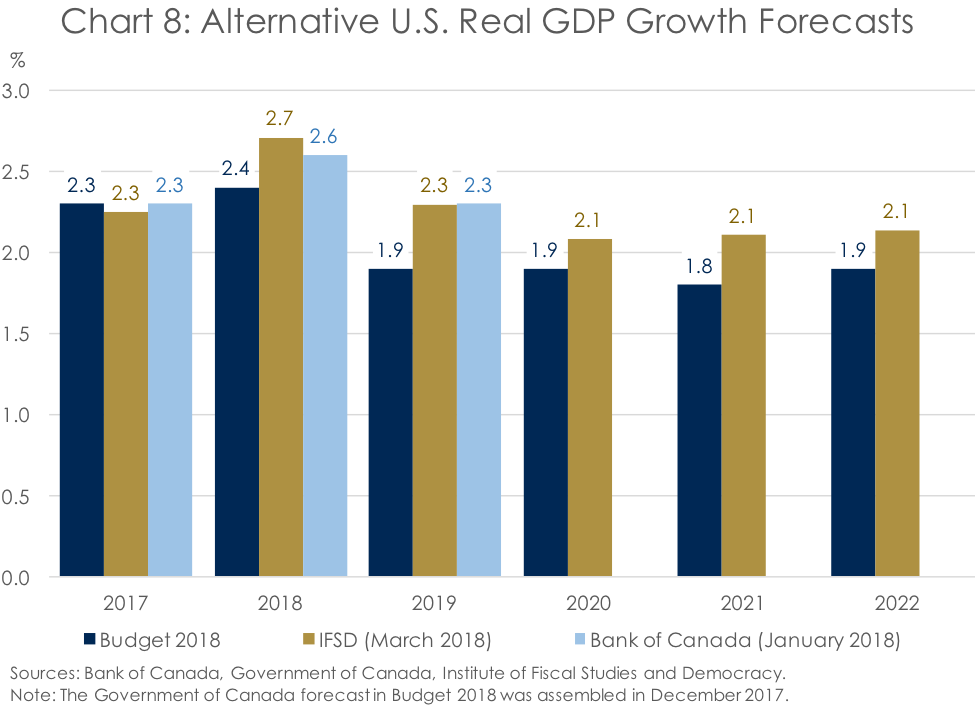

Looking more closely at the U.S. economy, the IFSD is projecting real GDP growth which is noticeably higher than that published in Budget 2018 (Chart 8; see Table A for the IFSD’s full U.S. economic forecast). But without additional detail on what is underneath the federal government forecast, it’s difficult to know what underlies this difference. However, given the survey of economists was undertaken in December 2017, and was hence well out of date when Budget 2018 was published, one can assume the difference reflects more recent economic data for 2017 and 2018 as well as the impact U.S. tax reforms passed in mid-late December 2017. Indeed, given the similarity between the U.S. real GDP growth forecasts of the IFSD and Bank of Canada, as well as the Consensus Economics survey, the forecast used in Budget 2018 should raise some eyebrows. As such, better-than-expected U.S. economic activity could be the source of a potential upside surprise for the federal government’s economic outlook. This is particularly the case as the IFSD took a relatively conservative approach to incorporating the recent U.S. tax reforms, opting for the lower end of a range of estimates. With that said, it is worth noting that, if the IFSD were to use the federal government’s U.S. real GDP growth forecast in its outlook, the IFSD’s forecast for Canadian economic activity would be more muted than that presented in Table B.

2019 May Be the Year Deficits Start Rising

So, with revenues likely to be on a lower track than was projected in Budget 2018, the question becomes: What response will this elicit from the feds? Will they stick to their current but questionable path for shrinking deficits and a falling debt-to-GDP ratio by cutting spending or will they turn on the fiscal taps under the auspices of investing in “middle class Canadians and those working hard to join them”?

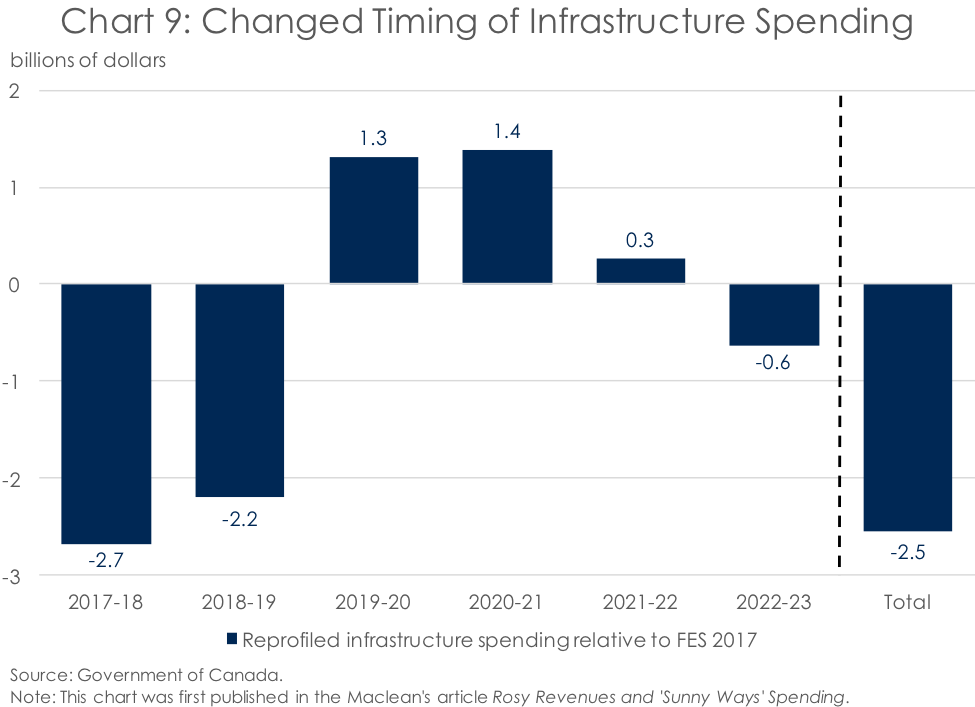

Certainly any boost to fiscal outlays isn’t going to come from additional spending on infrastructure, as the federal government has shown itself to be more adept at announcing ribbon-cutting photo-ops than actually getting shovels in the ground (Chart 9, originally published by Maclean’s). Instead, with Budget 2018 demonstrating that the feds are willing to run deficits to fund operating expenses and 2019 being an election year, it’s not unreasonable to expect a federal debt-financed spending binge to be in Canada’s near-term future.

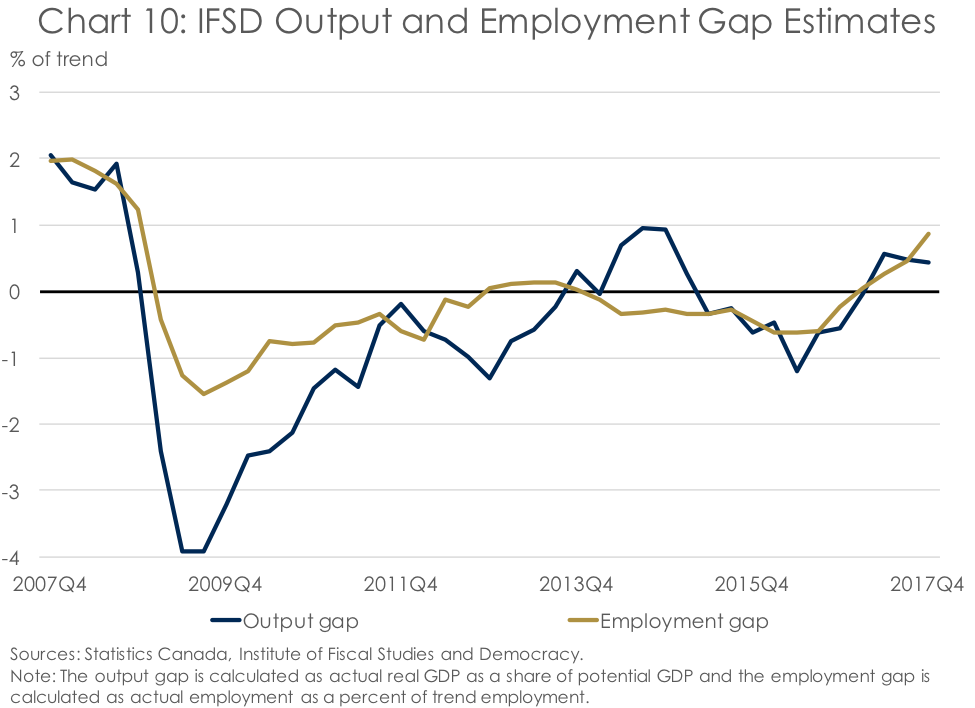

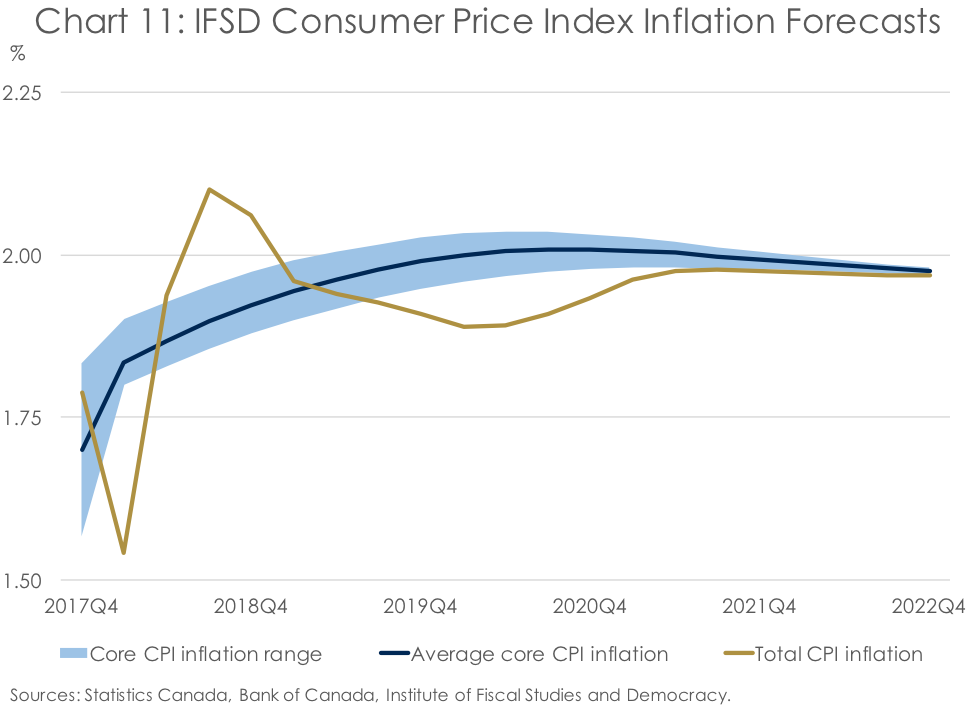

If it is the case that the federal government borrows heavily to ramp up spending in 2019, there are important implications for, as the Bank of Canada said recently, “… an economy operating near capacity … with no labour market slack” (Chart 10). The impact of fiscal largesse in this environment will largely take the form of higher wage and price inflation, which are already being realized (Chart 11). Indeed, according to multiple measures tracked by the Bank of Canada, year-over-year wage growth is well above 2%, and it isn’t expected to come down any time soon. And with higher inflation comes rising interest rates, which will have a cooling effect on the economic impacts any fiscal largesse meant to stimulate an economy which is already operating at its potential.

Conclusion

Against the backdrop of an economy back at its potential, inflation near its target, and still highly accommodative monetary policy, one would typically assume that prudent fiscal policy would be for the federal government to run surpluses in order to stuff its mattress for a rainy day. And with storm clouds on the horizon in the form of a plethora of downside economic risks, this should be even more so the case.

However, this is not the track taken by the federal government. Instead, it has opted to punt capital spending off to a future mandate so as to deficit-finance operating expenses today. Citing the debt-to-GDP ratio as a fiscal benchmark, Canadians are asked to take comfort in the hope that this benign economic and fiscal outlook will come true. However, we are already seeing that the economic outlook in Budget 2018, resulting from a survey taken in December 2017, is long out of date. As such, the storm clouds are getting closer and the feds are leaving us stuck outside without an umbrella.