Following the release of Statistics Canada’s March 2018 Labour Force Survey (LFS), the Institute of Fiscal Studies and Democracy (IFSD) has updated its Canada JØLTS for February 2018.

Economic and Monetary Implications

In February 2018, the unemployment outflow rate––the “speed” at which unemployed people find a job––decreased by 1%. Meanwhile, the inflow rate––the “speed” at which employed people lose or quit their job and go unemployed––increased by 1%. The drop in the outflow rate broadly offset the rise in the inflow rate. However, at the margin, the overall unemployment rate in Canada fell by 0.1 percentage point in February, from 5.9% to 5.8% (and then was stable at 5.8% in March).

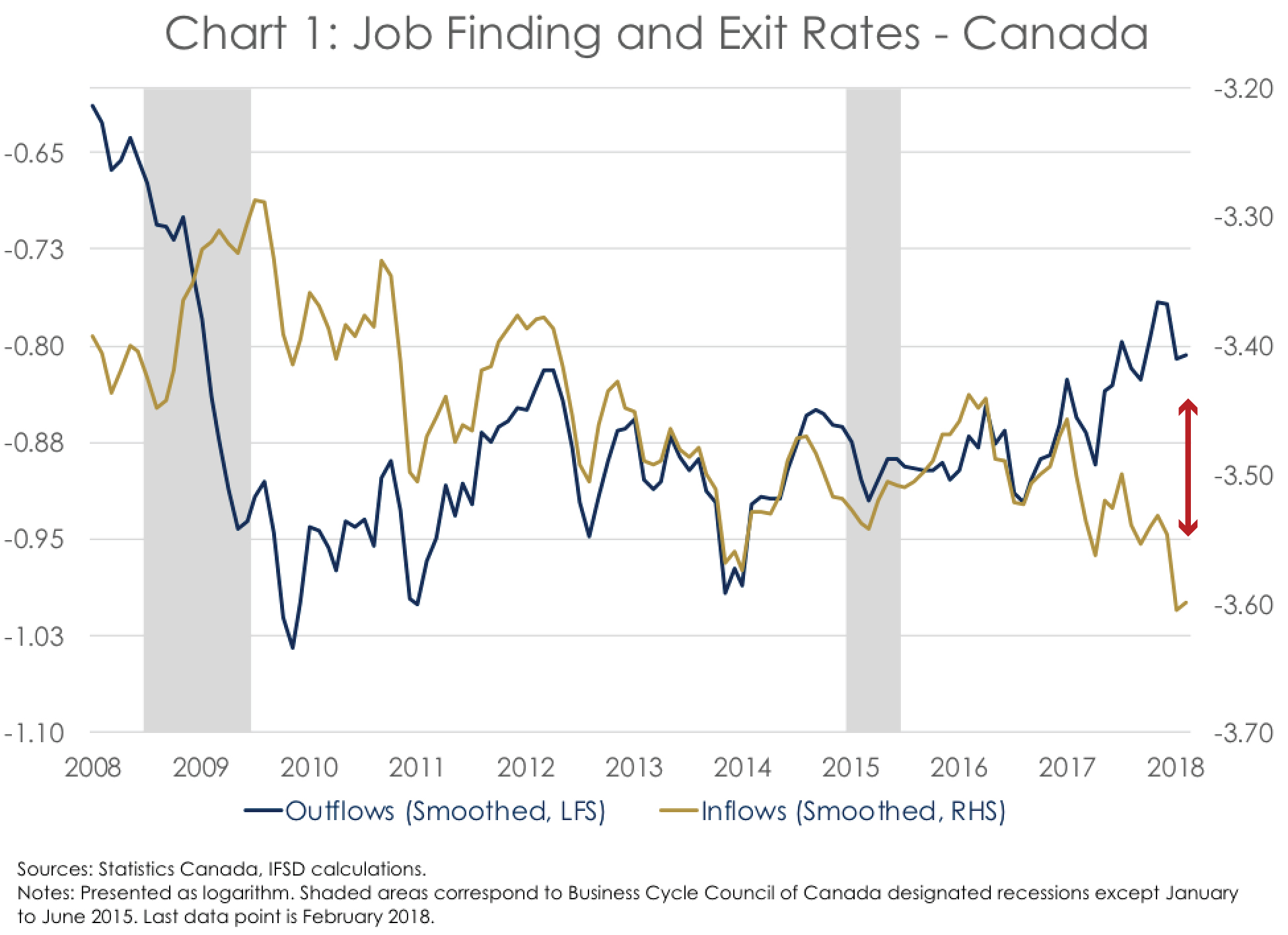

The Canada JØLTS for January and February 2018 point to a stabilization of the movements in and out of the unemployment pool after some weakness in outflows at the end of 2017 (Chart 1). That said, the trend illustrated by the 3-month moving average of the unemployment outflows and inflows is still intact, with the former firmly trending up since the end of 2016 and the latter trending down. The gap between the relative speeds at which 1) unemployed people are finding jobs and 2) employed people are losing or quitting jobs continues to support the idea that the labour market in the country is tight, with firms having increased difficulty filling vacant positions.

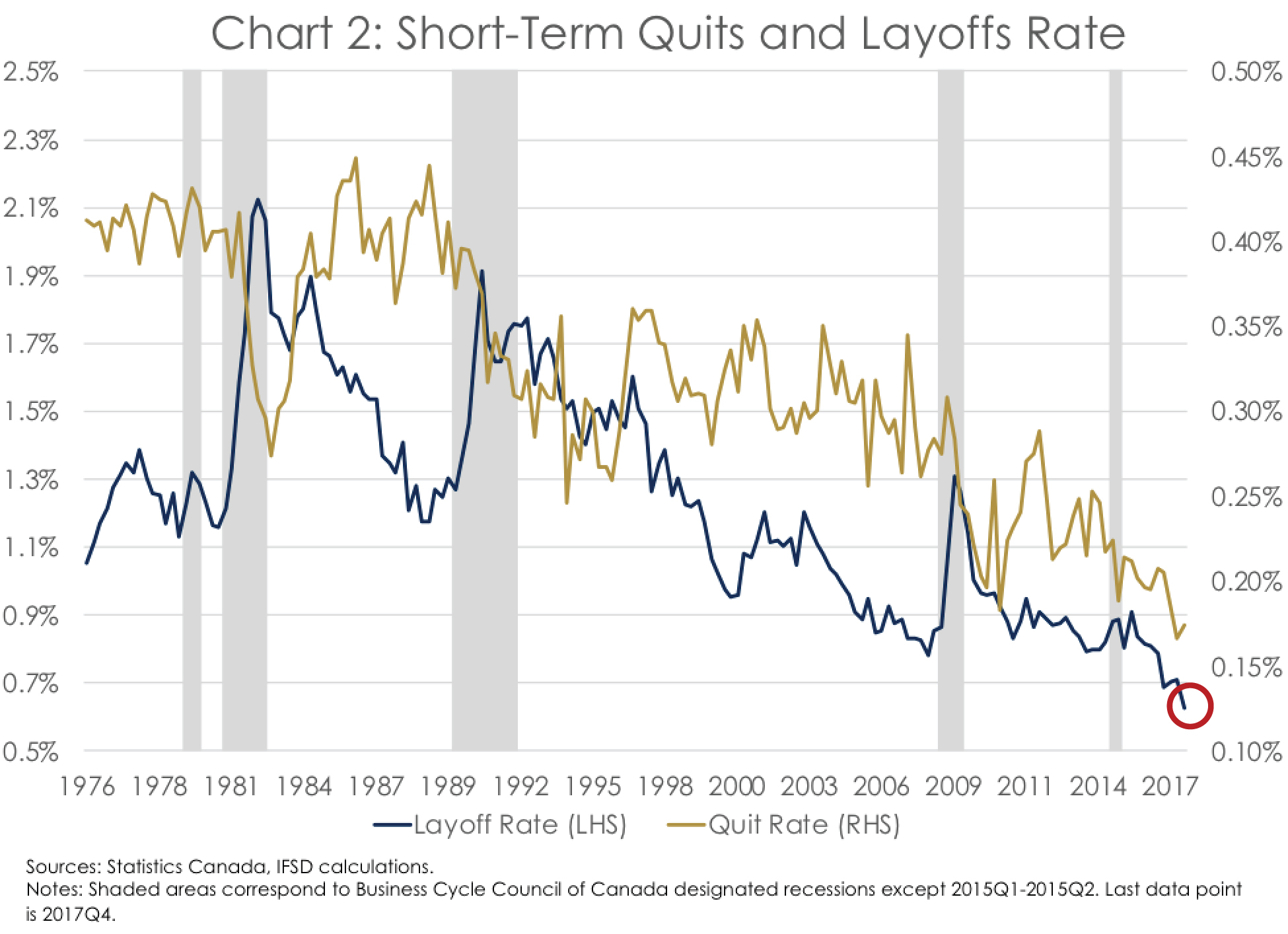

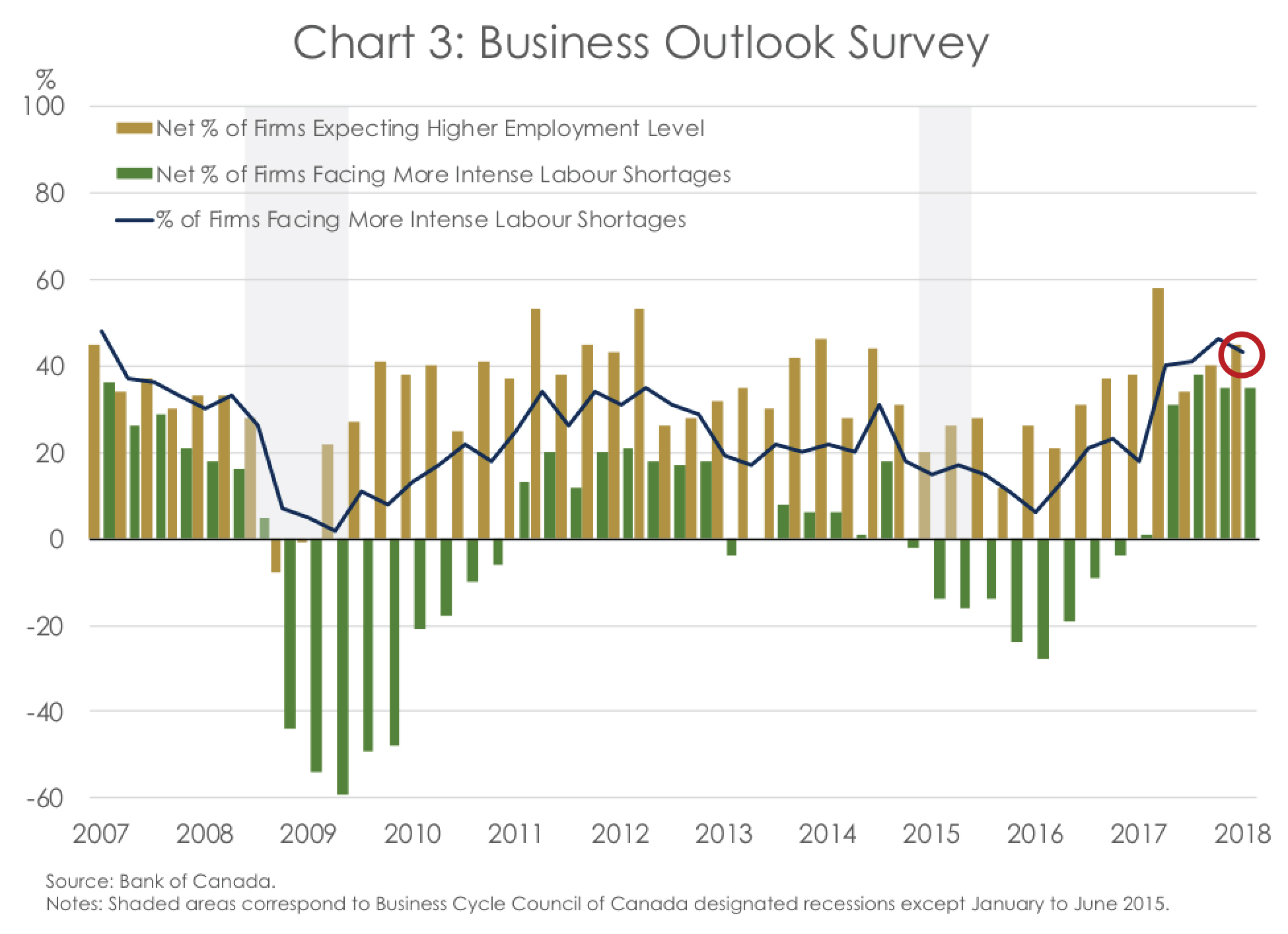

Several other labour market indicators support the view that there is little slack remaining in the Canadian labour market. First, in the fourth quarter of 2017, the IFSD’s estimated short-term layoff rate reached a new record low, at 0.6% of workers (Chart 2).[1] As the share of firms facing more intense labour shortages continues to hover near historical highs and as labour shortages become “evident in most regions” (per the Bank of Canada’s Q1 Business Outlook Survey), far fewer workers are experiencing layoffs (Chart 3). Moreover, the job vacancy rate, as measured in Statistics Canada’s Survey of Employment, Payrolls and Hours (SEPH), has exhibited a very steep increase since the end of 2016 (Chart 4).

|

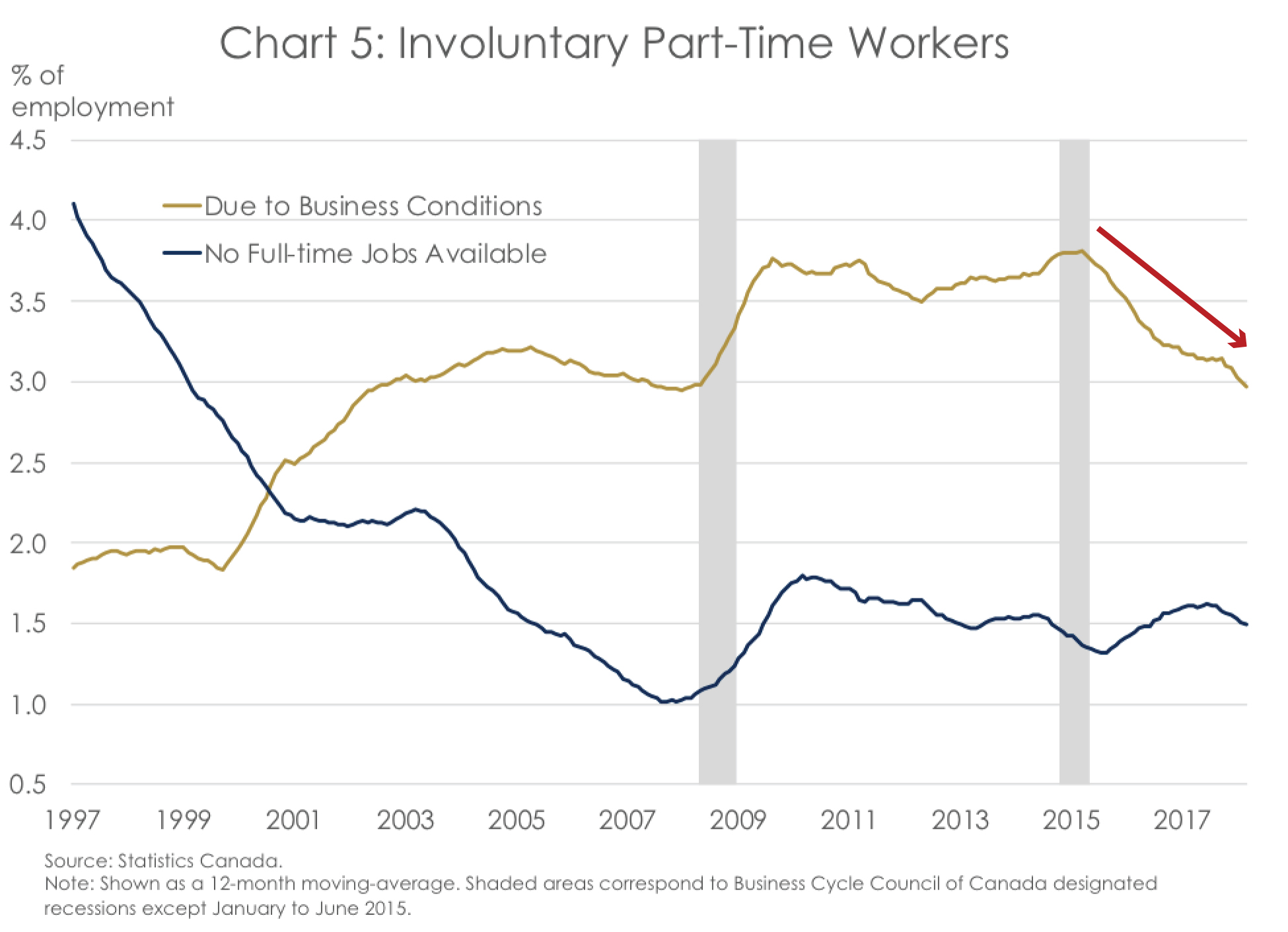

Finally, while some measures of pending labour market slack closely followed by the Bank of Canada have not yet reached their pre-recession levels, most have improved.[2] Notably, the incidence of people working part-time due to business conditions virtually reached its pre-recession lows in March 2018 (Chart 5). However, the incidence of part-time work due to a lack of full-time positions is still relatively high. In the context of the record high vacancy rates discussed above, we believe that this likely reflects a long-term structural factor (skills mismatch) as opposed to short-term cyclical factors (insufficient demand). It may also reflect the changing nature of work, although this is harder to conclude definitively.

|

||||

All in all, the pace of economic growth in the last three quarters has moderated towards the IFSD’s estimate of long-term potential GDP growth (1.6%) and the labour market has continued to display evidence of being at full employment. Considering this, we are still of the view that the Bank of Canada (BoC) is on a tightening path, but rate hikes will continue to be very gradual:

- While the BoC highlighted the tightness of the Canadian labour market in its most recent Monetary Policy Report, notably through wage gains, as mentioned above, it still sees labour market slack in some part of the economy.2

- The BoC forecasts 2.5% real GDP growth in 2018Q2 based on partial rebounds in exports and business investment. In the medium-term, those sectors are expected to grow in line with foreign demand. Given that such a scenario has fallen short of expectations in the last two years, there is likely less room for positive economic surprises that would bring forward the timing, numbers of rate hikes.

- The BoC Governor has mentioned that positive development related to NAFTA, which we believe is more likely than last quarter, would need to be accompanied by some improvement in economic data in order to alter the path for interest rates.

Given this, while May is still possible, the IFSD believes that the next interest rate hike will come in July, followed by another one in October.

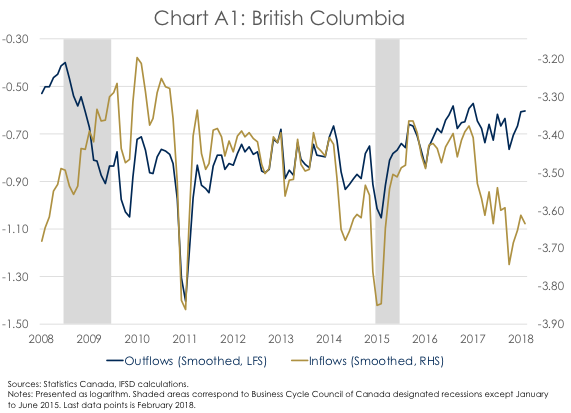

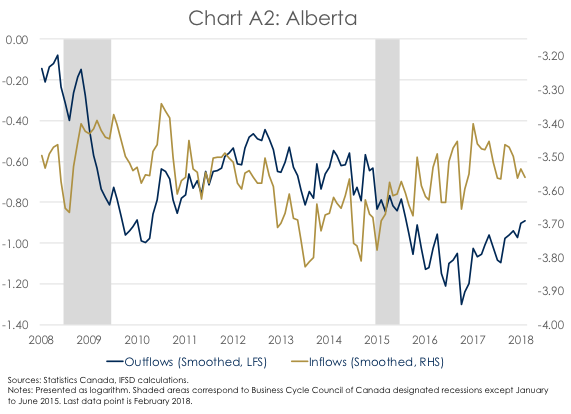

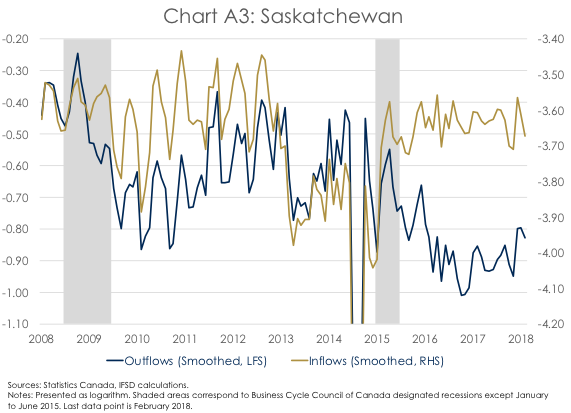

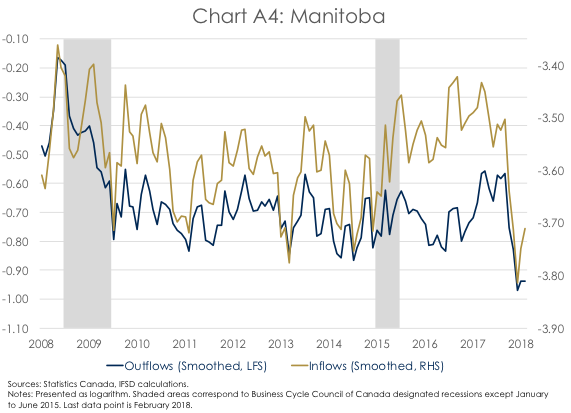

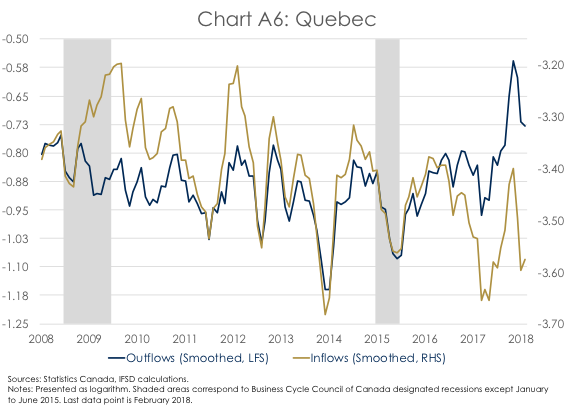

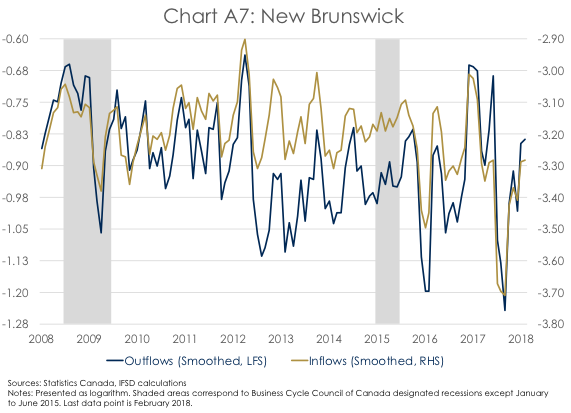

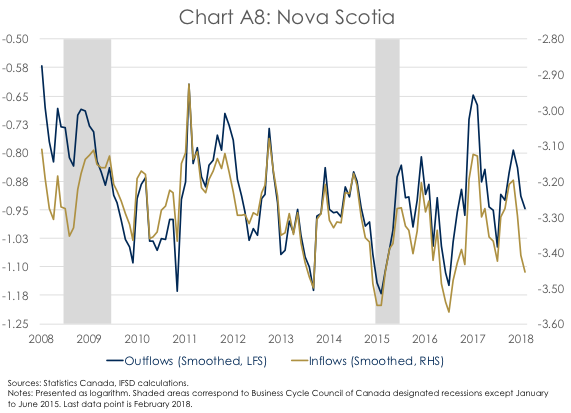

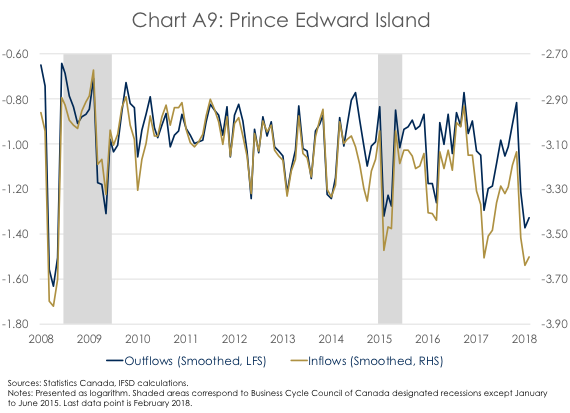

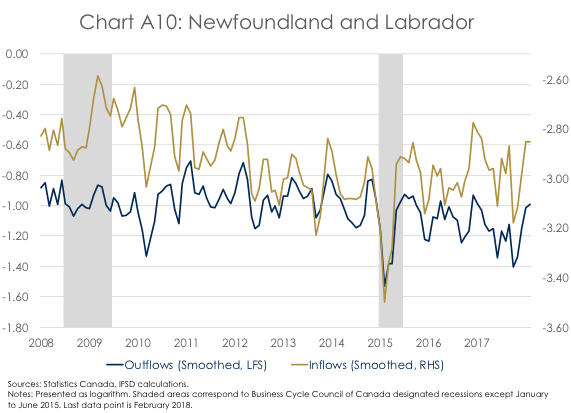

Annex 1 – Provincial JØLTS

[1] In the fourth quarter of 2017, the quit rate was also very low at 0.2%.

[2] See, for example, the Bank of Canada labour market indicator and the long-term unemployment rate and youth participation rate (Box 3 of the Bank of Canada April 2018 Monetary Policy Report).